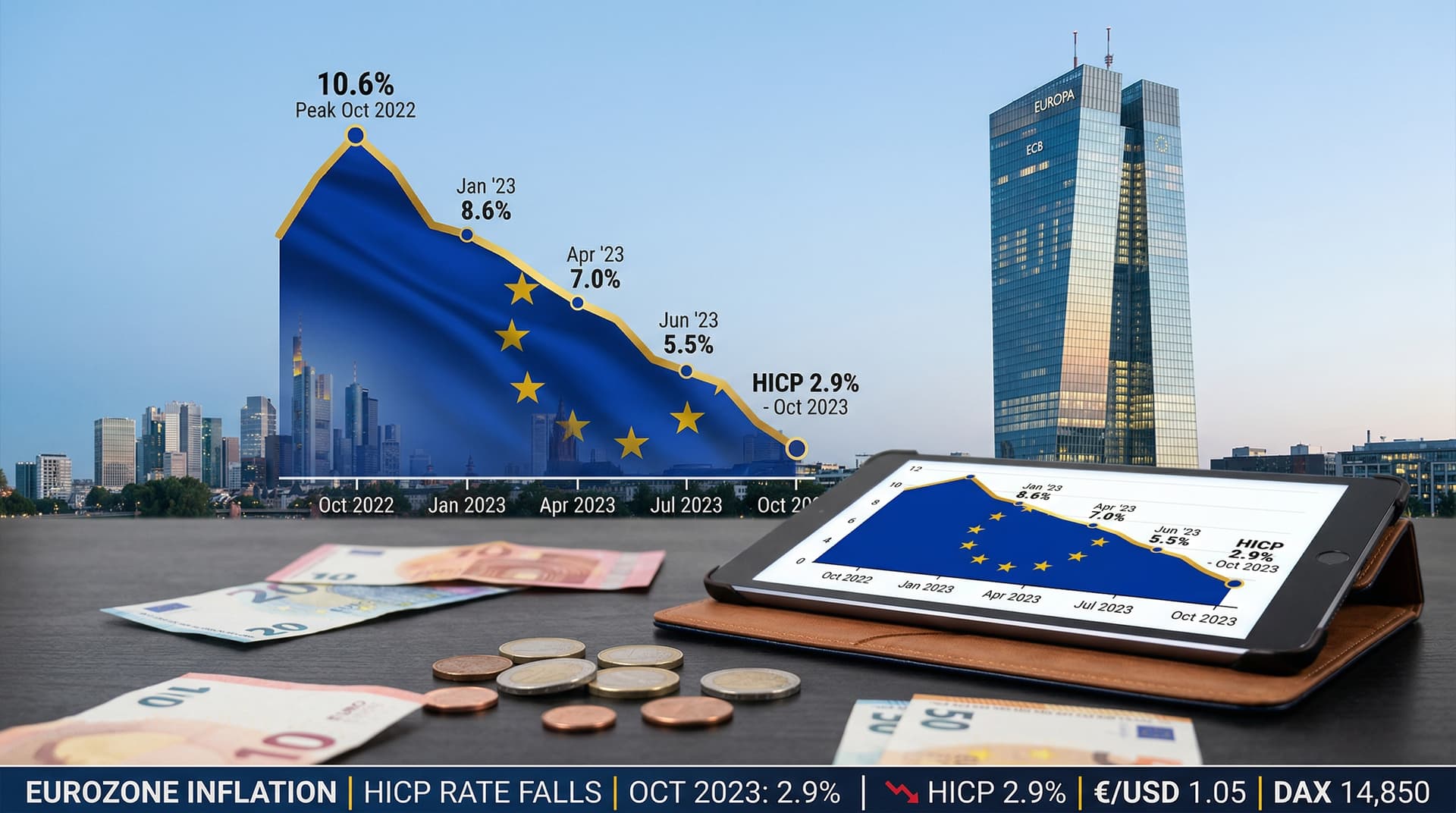

In a significant relief for European policymakers and households alike, inflation across the euro area plummeted to 2.9% in October 2023, marking the lowest level since July 2021. Eurostat, the EU's statistical office, released the flash estimate on October 31, showing a sharp decline from September's 4.3%. This data, confirmed in early November reports, underscores a cooling of price pressures that have plagued the region since Russia's invasion of Ukraine triggered energy shocks.

Breakdown of the Numbers

The headline Harmonised Index of Consumer Prices (HICP) figure of 2.9% year-on-year reflects a broad-based slowdown. Energy prices, which had been a major driver of inflation earlier in the year, fell by 2.3%, providing substantial relief after months of volatility. Non-energy industrial goods inflation eased to 0.5%, while services—a stubborn component—dropped to 4.0% from 4.5%.

Core inflation, excluding volatile energy and unprocessed food, stood at 4.2%, down from 4.5% in September. This measure, closely watched by the European Central Bank (ECB), indicates underlying pressures are also abating, though still above the bank's 2% medium-term target.

Country-level data paints a varied picture. Germany's inflation rate slid to 3.8% from 4.5%, France saw a dip to around 4.0%, and Italy's figure fell to 1.7%. Spain, however, remained higher at 3.5%, highlighting regional disparities influenced by national energy policies and wage dynamics.

| Indicator | October 2023 | September 2023 | Change |

|---|---|---|---|

| Headline HICP YoY | 2.9% | 4.3% | -1.4 pts |

| Core HICP YoY | 4.2% | 4.5% | -0.3 pts |

| Energy YoY | -2.3% | 5.8% | -8.1 pts |

| Services YoY | 4.0% | 4.5% | -0.5 pts |

Context: From Peak to Trough

Eurozone inflation peaked at 10.6% in October 2022, fueled by surging natural gas prices following the curtailment of Russian supplies. The ECB responded aggressively, hiking its deposit rate from negative territory to 4% by September 2023—the fastest tightening cycle in its history. These measures, combined with fiscal support like the EU's temporary crisis framework allowing higher deficits, have finally bent the inflation curve downward.

Milder winter weather, strategic gas storage fills ahead of schedule, and diversified LNG imports have stabilized energy markets. Wholesale gas prices, which hit €300/MWh last summer, have retreated below €50/MWh as of early November. However, challenges persist: food inflation lingers at 4.5%, and wage growth in tight labor markets could reignite services inflation.

ECB Policy Outlook

The data arrives ahead of the ECB's December 14 Governing Council meeting, intensifying debates on rate trajectory. President Christine Lagarde has emphasized data-dependence, stressing that policy must remain restrictive until inflation sustainably hits 2%. Yet, with headline inflation now just 0.9 points above target and projections showing further declines, markets are pricing in a 25 basis point cut in December, with more easing in 2024.

Economists at ING and Deutsche Bank note the October print reduces upside risks, potentially allowing a pivot. However, sticky core inflation warrants caution—Lagarde reiterated in recent speeches that premature easing could undo progress. The ECB's latest staff projections from September foresaw inflation averaging 5.3% in 2023, dropping to 2.4% in 2025; today's data supports a downward revision.

Broader Economic Implications

For households, the slowdown means less erosion of purchasing power. Real disposable incomes, squeezed since 2022, may stabilize, supporting consumption—a key growth driver. Eurozone GDP grew 0.1% in Q3 2023 after a flat Q2, per early estimates, but faces headwinds from high borrowing costs and weak external demand.

Manufacturing PMI surveys in October signaled ongoing contraction, with the index at 43.1, while services held above 50. Germany's industrial output fell 0.8% in September, underscoring the auto sector's struggles amid high rates and Chinese EV competition. In finance, bond yields dipped post-data: the 10-year Bund yield fell to 2.65% from 2.75%.

Fiscal policy plays a role too. France and Italy face scrutiny under the EU's Stability and Growth Pact, with debt-to-GDP ratios above 100%. The Commission's November economic forecast, due soon, will incorporate this inflation relief, potentially easing deficit pressures.

Risks and Forward Look

Downside risks include geopolitical tensions—Middle East conflicts could spike oil prices, currently around $85/barrel—and China's property woes dampening exports. Upside pressures: labor shortages pushing wages up 4-5% annually.

Looking to November data, due mid-month, analysts expect further softening. If trends hold, the ECB could signal a pause or cut by year-end, boosting equities and easing mortgage burdens. European stocks, via the STOXX 600, rose 0.5% on the inflation news, with banks gaining on lower rate hike odds.

This inflection point offers hope after 18 months of pain. Yet, as ECB Chief Economist Philip Lane noted, 'disinflation is not yet won.' Policymakers must balance growth revival with price stability in a fragile recovery.

In sum, October's 2.9% print is a milestone, signaling the end of the acute phase of Europe's inflation saga. For businesses, investors, and citizens, it paves the way for normalization—though vigilance remains key in an interconnected global economy.

Europe World News, November 6, 2023